What are the next steps after company incorporation in Poland?

Successfully finishing your company incorporation in Poland is just the beginning. The newly registered LLC, which according to 94% of investors’ preferences gains a separate legal personality, must immediately fulfill strict official requirements. The management board faces the obligation to complete crucial fiscal, accounting, and registry formalities.

Ignoring these guidelines risks heavy financial penalties imposed by the state. The following article clearly explains the deadlines associated with NIP-8 declarations, VAT-R, reporting ultimate beneficial owners to the CRBR, and paying the PCC-3 capital tax, ensuring full post-registration compliance.

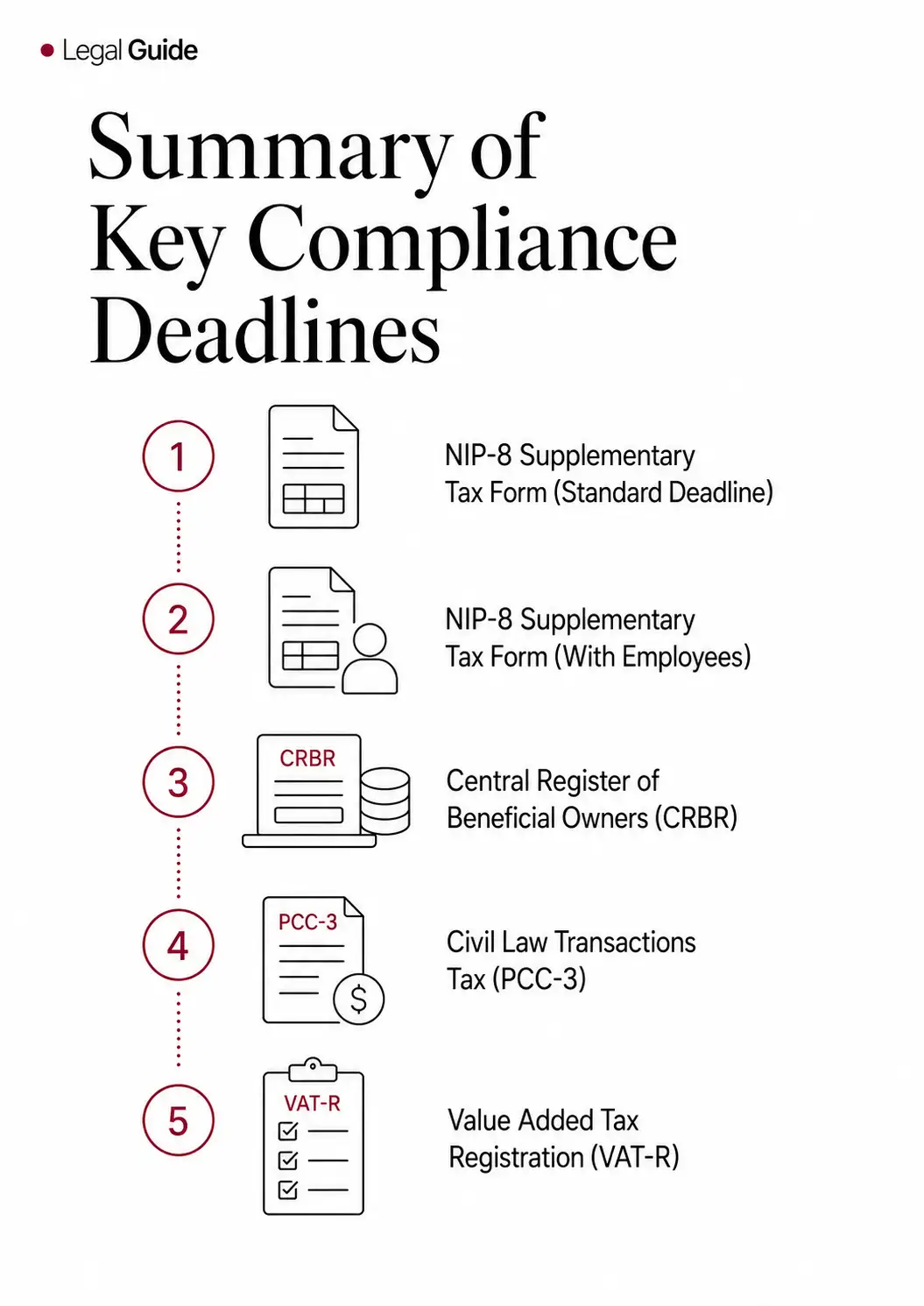

Summary of Key Compliance Deadlines

To maintain operational legality, foreign founders must adhere to the following statutory registration and tax deadlines immediately upon entry into the National Court Register (KRS):

NIP-8 Supplementary Tax Form (Standard Deadline)

The standard deadline to submit the NIP-8 form to the tax office is 21 days from the company’s official KRS registration date. This form is mandatory for disclosing supplementary corporate data, such as bank account numbers and the exact location of accounting books.

NIP-8 Supplementary Tax Form (With Employees)

If the newly formed company intends to hire personnel and incurs immediate social security obligations, the submission deadline for the NIP-8 form is drastically shortened to 7 days from the KRS registration entry.

Central Register of Beneficial Owners (CRBR in Poland)

The management board must officially report all Ultimate Beneficial Owners (individuals holding more than 25% of shares or voting rights) to the CRBR within a strict limit of 14 days from the court registration.

Civil Law Transactions Tax (PCC-3 in Poland)

The company must settle a one-time 0.5% civil law transactions tax on its share capital within 14 days from the date of executing the Articles of Association.

Value Added Tax Registration (VAT-R in Poland)

The VAT-R registration application must be filed and processed before the company executes its very first taxable sale or service delivery to secure active VAT or EU-VAT status.

When must the NIP-8 form be submitted to the tax office?

From the moment the company is registered in the Polish court (KRS), basic data such as the NIP (tax identification number) or REGON are assigned automatically through the “one-stop-shop” system.

However, there is a strict obligation to provide supplementary data to the tax administration. This is exactly what the special NIP-8 official form is for, covering information such as corporate bank account numbers and exact places of business operations.

The timeframe for submitting this notification is tightly regulated by law.

- Standardly, a company has 21 days to submit the NIP-8 form, counting from the date of KRS entry.

- One must stay vigilant, though – if the company hires employees and reports social security obligations, this deadline is drastically shortened to just 7 days.

Failing to report this information blocks the company’s full legal operation in fiscal relations.

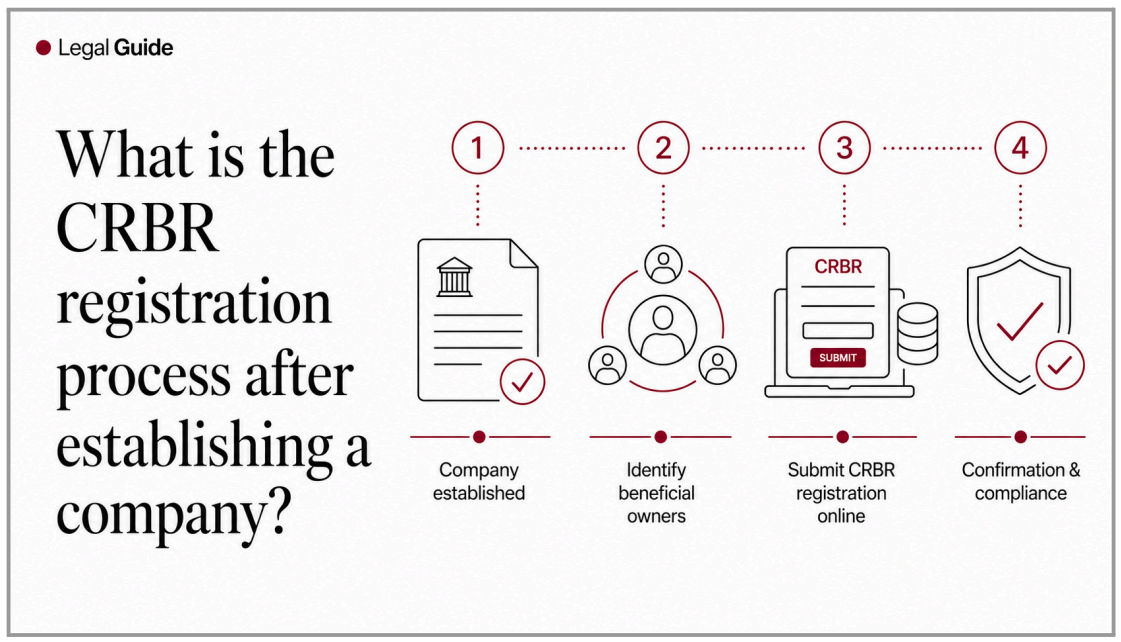

What is the CRBR registration process in Poland after establishing a company?

The Central Register of Beneficial Owners (CRBR) is a Polish system designed to prevent money laundering and counter terrorism financing (AML directives). A newly registered company is strictly obligated to disclose the natural persons who exercise direct or indirect ownership control over it. This primarily applies to shareholders controlling more than 25% of the company’s capital.

The deadline to report the structure to the Register is only 14 days from the moment the company is registered in the KRS. The submission is done entirely electronically, but it requires the signatures of board members by the company’s representation rules. Failure to make a timely entry in the CRBR is punishable by extremely severe sanctions, which can reach up to 1 million PLN imposed directly on the economic entity.

How to handle VAT-R registration and the PCC-3 tax?

In addition to basic data, every new company engaging in the active sale of services or goods must obtain the status of an active VAT taxpayer. This is achieved through the registration process using the VAT-R form. The declaration must be submitted before executing the first taxable transaction. Importantly, foreign entrepreneurs operating within the EU often also apply for EU-VAT status for intra-community transactions.

Another one-time tax obligation following incorporation is the civil law transactions tax related to the share capital. This tax, known as PCC-3, must be settled within 14 days from the signing of the Articles of Association and amounts to 0.5% of the declared capital value, minus the notarial act costs. For companies formed electronically (S24), the fee must be paid independently to the Tax Office, whereas, at a Notary, this tax is usually collected and remitted by the law office itself.

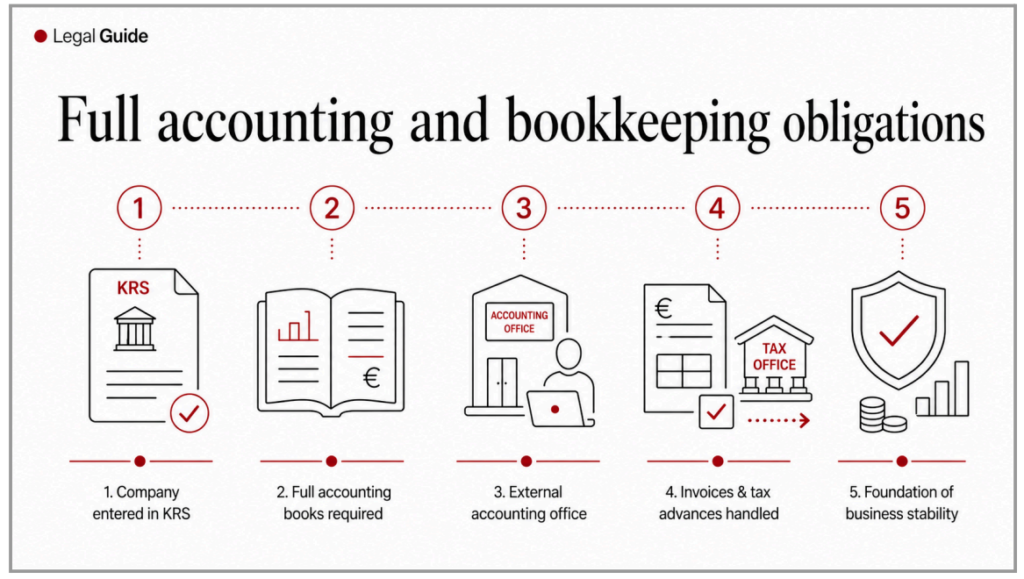

Full accounting and bookkeeping obligations in Poland

With the official entry into the KRS list, the full weight of maintaining professional accounting matters falls on the company’s shoulders. Limited Liability Companies are subject to the obligation of keeping full accounting (so-called full accounting books).

This usually requires engaging an external accounting office (outsourcing) responsible for properly booking invoices and remitting timely tax advances to the tax office on behalf of the board. Proper tax handling is the foundation of business stability in Poland.

Next steps after company incorporation in Poland – FAQ

How to submit supplementary data?

After obtaining the KRS entry, the company has 21 days to submit the NIP-8 form to the tax office, disclosing details like the bank account number and the location where accounting books are kept.

What is the CRBR and what is the registration deadline?

The CRBR is the state Central Register of Beneficial Owners. A company must report its main shareholders (holding >25%) within a strict deadline of 14 days from registration.

How is the share capital taxed in Poland?

The company’s share capital (minimum 5,000 PLN) is subject to a one-time civil law transactions tax (PCC-3) of 0.5%, which must be paid to the tax office within 14 days.

When do I become an active VAT payer?

Obtaining an automatic NIP number does not mean the company has active VAT status. A separate VAT-R document must be submitted before the board makes its first sale.

Does the company need full accounting in Poland?

Yes, the legal form of a Limited Liability Company imposes a statutory obligation on the board to maintain rigorous, full accounting records (books of accounts).

Recommended institutions

Company’s partner

Institution name

Company’s partner

Institution name

Company’s partner

Institution name

Company’s partner

Institution name

Company’s partner

Institution name

Company’s partner

Institution name

Recommended lawyers

Barrister | Managing Partner

Zbigniew

Lorem

READ MORE

Barrister | Managing Partner

Władysław

Ipsum

READ MORE

Barrister | Managing Partner

Mirosław

Lorem

READ MORE

Barrister | Managing Partner

Mirosław

Lorem

READ MORE